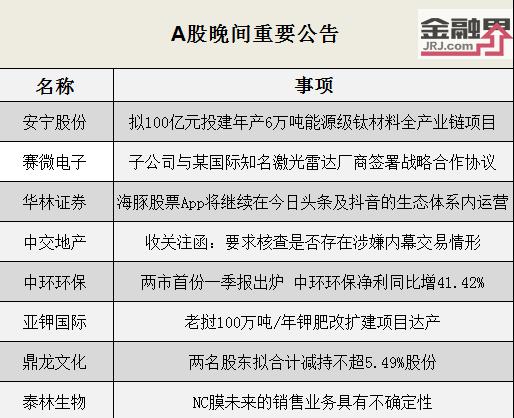

News from the financial sector on April 1 ST, the important announcement was read first this evening-CCCC Real Estate received a letter of concern asking to check whether there was any suspected insider trading, Anning Co., Ltd. planned to invest 10 billion yuan to build a whole industrial chain project with an annual output of 60,000 tons of energy-grade titanium materials, and Saimicroelectronics subsidiary signed a strategic cooperation agreement with an internationally renowned laser radar manufacturer …

[Hot Spots]

*ST Deao: reported to the public security organ that Wang Xinwen, then the legal representative, was suspected of violating the law and committing crimes.

*ST Deao announced that due to the financial dispute with Guangzhou Rural Commercial Bank, the company undertook the obligation to make up the difference for the trust loan of 2.5 billion yuan provided by Guangzhou Rural Commercial Bank to Huaxiang (Beijing) Investment Co., Ltd. The case was decided in the first instance. On January 30th, the company received the Civil Judgment issued by Guangzhou Intermediate People’s Court, ruling that the company should be liable for compensation. According to the case file, the copy of the Balance Supplement Agreement provided by Guangzhou Rural Commercial Bank was signed and sealed on behalf of the company as the legal representative at that time, Wang Xinwen. In order to safeguard the legitimate rights and interests of the company, on March 30, the company reported to the public security organ that Wang Xinwen, then the legal representative, was suspected of violating the law and committing crimes. On March 31st, the company received a receipt from Nanhai District Public Security Bureau of Foshan City, and the case has been accepted.

Letter of concern from CCCC Real Estate: Request to check whether there is any suspected insider trading.

CCCC Real Estate (000736) received a letter of concern from Shenzhen Stock Exchange, requesting to check whether the controlling shareholders, actual controllers, directors, supervisors, senior executives and their immediate family members of the company have bought or sold the company’s shares and whether there is any suspected insider trading. Explain in detail the recent investigation by reception institutions and individual investors, whether the undisclosed annual report information of the company is provided to a third party other than the annual audit accounting firm, and whether there is any violation of fair disclosure of information.

Xinzhu shares: the concerted action of the controlling shareholder intends to increase its shares.

Xinzhu Co., Ltd. (002480) announced on the evening of April 1 that Sichuan Development, the controlling shareholder of the company, intends to designate the Sichuan Relief Development Fund managed by Sichuan Development Securities Fund under its control to increase its shareholding in the company by centralized bidding. The number to be increased is no more than 3,768,500 shares (accounting for 0.49% of the company’s total share capital) and no less than 1,884,200 shares; The implementation period is completed within 6 months from the date of announcement of the increase plan.

Chuanfa Longman: The concerted action of the controlling shareholder plans to increase its shareholding by RMB 200 million to RMB 300 million.

Chuanfa Longman (002312) announced on the evening of April 1 that Sichuan Development Securities Fund, the concerted action of Sichuan Advanced Materials Group, the controlling shareholder of the company, intends to designate the Sichuan Relief Development Fund under its control to increase the company’s shares through centralized bidding, with an increase of not less than 200 million yuan and not more than 300 million yuan, which will be completed within 6 months from the date of announcement of the increase plan.

Vanke A: Wanwuyun submitted a listing application to the Hong Kong Stock Exchange.

Vanke A (000002) announced on the evening of April 1 that Wanwuyun, a subsidiary of the company, submitted its listing application to the Hong Kong Stock Exchange through its co-sponsors on March 31. The overseas spin-off and listing of Wanwuyun must be approved by the China Securities Regulatory Commission, the Hong Kong Stock Exchange and other relevant regulatory agencies, and market conditions and other factors should be taken into account before it can be implemented.

[Financing and fixed increase]

Xinjiang Tianye: The application for public offering of convertible bonds was approved.

On April 1st, the public offering of convertible corporate bonds by Xinjiang Tianye (600075) was approved by the CSRC. According to the data, the Xinjiang Tianye convertible bonds will raise no more than 3 billion yuan, and it is planned to invest in two green and efficient resin circular economy industrial chain projects with an annual output of 250,000 tons of ultra-clean high-purity alcohol-based fine chemicals and high-performance resins, as well as to supplement working capital.

Shenma shares: the proposed convertible bonds will raise no more than 3 billion yuan.

Shenma Co., Ltd. (600810) announced on the evening of April 1 that it plans to issue convertible bonds to raise no more than 3 billion yuan, which will be used for supporting hydrogen and ammonia projects in nylon chemical industry, projects with an annual output of 240,000 tons of bisphenol A, supplementary liquidity and repayment of bank loans.

Aerospace Changfeng: It is planned to raise no more than 325 million yuan.

Aerospace Changfeng (600855) announced on the evening of April 1 that it plans to raise no more than 325 million yuan for the verification capacity building project of energy storage power supply, the development and production capacity improvement project of domestic high-power density module power supply, the development and industrialization project of integrated border and coastal defense detection equipment and system platform based on artificial intelligence, the research and development capacity improvement project of customized infrared thermal imager and supplementary liquidity.

【 Operation and Performance 】

Hongqi Chain: The net profit in 2021 decreased by 4.66% year-on-year, and it is planned to be 0.14 yuan for 10 shares.

Hongqi Chain (002697) disclosed its annual report on the evening of April 1, and achieved an operating income of 9.351 billion yuan in 2021, a year-on-year increase of 3.29%; The net profit was 481 million yuan, down 4.66% year-on-year; The basic earnings per share is 0.35 yuan. The company plans to distribute a cash dividend of 0.14 yuan (including tax) for every 10 shares.

Three Gorges Energy: Total power generation in the first quarter increased by 46.58% year-on-year.

Three Gorges Energy (600905) announced on the evening of April 1 that the company’s total power generation in the first quarter of 2022 was 11.631 billion kWh, an increase of 46.58% over the same period of last year. Among them, wind power generated 8.567 billion kWh, a year-on-year increase of 47.99%; Solar energy generated 2.963 billion kWh, up 44.18% year-on-year; Hydropower generated 101 million kWh, up 10.99% year-on-year.

Yi Delong: The net profit in 2021 was 227 million yuan, a year-on-year increase of 37.33%.

Yi Delong (603380) disclosed its annual report on the evening of April 1, and the company achieved an operating income of 1.752 billion yuan in 2021, a year-on-year increase of 35.88%; The net profit was 227 million yuan, a year-on-year increase of 37.33%; The basic earnings per share is 1.42 yuan. The company plans to distribute a cash bonus of 1.9 yuan (including tax) for every 10 shares.

Jinfeng Liquor Industry: The net loss in 2021 was 12,845,800 yuan.

Jinfeng Liquor Industry (600616) disclosed its annual report on the evening of April 1, and the company achieved an operating income of 649 million yuan in 2021, a year-on-year increase of 6.83%; The net profit loss was 12,845,800 yuan, compared with the profit of 12,239,700 yuan in the same period of last year. The company plans to distribute a cash bonus of 0.3 yuan (including tax) for every 10 shares.

The first quarterly report of the two cities was released: the net profit of environmental protection in Central increased by 41.42% year on year.

Central Environmental Protection (300692) disclosed a quarterly report on the evening of April 1, and realized an operating income of 241 million yuan in the first quarter, up 33.79% year-on-year; The net profit was 45.3993 million yuan, a year-on-year increase of 41.42%; The basic earnings per share is 0.11 yuan.

Yuexiu Financial Holdings: In 2021, the net profit decreased by 46.25% year-on-year, and it is planned to send 2 yuan from 10 to 3.5.

Yuexiu Financial Holdings (000987) disclosed its annual report on the evening of April 1, and achieved an operating income of 13.314 billion yuan in 2021, a year-on-year increase of 37.44%; The net profit was 2.48 billion yuan, a year-on-year decrease of 46.25%; The basic earnings per share is 0.67 yuan. The company plans to increase 3.5 shares for every 10 shares and distribute the bonus 2 yuan (including tax).

CNPC Capital: The net profit in 2021 decreased by 29.24% year-on-year, and it is planned to pay 1.32 yuan for 10 shares.

CNPC Capital (000617) disclosed its annual report on the evening of April 1, and achieved a total operating income of 30.964 billion yuan in 2021, a year-on-year increase of 2.78%; The net profit was 5.55 billion yuan, a year-on-year decrease of 29.24%; The basic earnings per share is 0.44 yuan. The company plans to distribute a dividend of 1.32 yuan (including tax) for every 10 shares.

Seven wolves: the net profit in 2021 was 231 million yuan, up 10.65% year-on-year.

Seven wolves (002029) disclosed its annual report on the evening of April 1, and achieved an operating income of 3.514 billion yuan in 2021, a year-on-year increase of 5.52%; The net profit was 231 million yuan, a year-on-year increase of 10.65%; The basic earnings per share is 0.32 yuan.

Yaoji Technology: It is estimated that the net profit in the first quarter will drop by 50%-60% year-on-year.

Yaoji Technology (002605) disclosed its performance forecast on the evening of April 1, and estimated its net profit in the first quarter of 2022 to be 80-100 million yuan, down 50%-60% year-on-year. The main reason for the decline in performance: In order to promote the healthy development of new and old products in the mobile game business, the company has increased its efforts in combination with market conditions, and the estimated promotion expenses in the first quarter increased by about 50% year-on-year; The company continued to increase the R&D investment in the mobile game business, constantly updated the iterative upgrade version and developed new games. It is estimated that the R&D expenses in the first quarter will increase by about 35% year-on-year.

Dalian Heavy Industry: The net profit in the first quarter increased by 119.87%-185.83%.

Dalian Heavy Industry (002204) released its performance forecast on the evening of April 1st, and it is estimated that the net profit for the first quarter will be 60-78 million yuan, up 119.87-185.83% year-on-year. From January to March 2022, the company’s operating income is expected to reach more than 2.1 billion yuan, which is expected to increase by more than 20% year-on-year. In particular, the operating income of environmental protection intelligent coke oven machinery products and crane products has increased significantly year-on-year, driving the company’s overall profit to rise.

Rheinland Bio: It is estimated that the net profit in the first quarter will increase by 53.25%-81.11% year on year.

Rheinland Bio (002166) disclosed its performance forecast on the evening of April 1st, and estimated its net profit in the first quarter of 2022 to be 33-39 million yuan, up 53.25%-81.11% year-on-year. During the reporting period, the company continued to strengthen the market expansion of major varieties such as natural sweeteners and tea extracts, and further strengthened the company’s cost control and improvement, making the growth rate of net profit higher than the growth rate of operating income.

Tomson Bianjian: The net profit in the first quarter dropped by 10%-30% year-on-year.

Tomson Bianjian (300146) announced on the evening of April 1 that it expected a net profit of 571-735 million yuan in the first quarter, down 10%-30% year-on-year.

Merchants Highway: In 2021, the net profit will increase by 123.74% year-on-year, and it is planned to pay 3.46 yuan for 10 projects.

China Merchants Highway (001965) disclosed its annual report on the evening of April 1, and achieved an operating income of 8.626 billion yuan in 2021, a year-on-year increase of 22.03%; The net profit was 4.973 billion yuan, a year-on-year increase of 123.74%; The basic earnings per share is 0.77 yuan. The company plans to distribute a dividend of 3.46 yuan (including tax) for every 10 shares.

Huaibei Mining: The net profit in the first quarter increased by about 34.83% year-on-year.

Huaibei Mining (600985) announced on the evening of April 1 that its net profit in the first quarter is expected to be around 1,609.5 million yuan, up by 34.83% year-on-year. During the reporting period, the domestic coal market demand was strong, the energy price in the international market continued to rise, and the price of the company’s commercial coal increased compared with the same period; The company’s commercial coal sales increased slightly compared with the same period.

Guojin Securities: The net profit in 2021 was 2.317 billion yuan, a year-on-year increase of 24.41%.

Guojin Securities (600109) released a performance report on the evening of April 1, and its operating income in 2021 was 7.127 billion yuan, a year-on-year increase of 17.55%; The net profit was 2.317 billion yuan, a year-on-year increase of 24.41%; The basic earnings per share is 0.77 yuan.

[Investment, project bid]

Potassium International: Laos’ 1,000,000-ton/year potash fertilizer reconstruction and expansion project reaches production.

Potassium International (000893) announced on the evening of April 1 that the company’s 1 million tons/year potash fertilizer reconstruction and expansion project in Laos has achieved stable production, reaching the production capacity and product quality planned in the project design. The company disclosed its annual report on the same day, and achieved an operating income of 833 million yuan in 2021, a year-on-year increase of 129.36%; The net profit was 895 million yuan, a year-on-year increase of 1401.43%; The basic earnings per share is 1.18 yuan.

Yili Jieneng: It is planned to set up two joint ventures with Ordos in Three Gorges.

Yili Jieneng (600277) announced on the evening of April 1st that the company plans to sign a cooperation investment agreement with Three Gorges Erdos to jointly engage in photovoltaic sand control, hydrogen energy and energy storage industry management: the company plans to jointly invest with Three Gorges Erdos to set up two joint ventures-Inner Mongolia Three Gorges Yili New Energy Co., Ltd. and Wuwei Xintengli Ecological Energy Technology Co., Ltd.. Each company plans to have a registered capital of 1.4 billion yuan, and the company holds 50% of the shares, which is an associated company.

Saimicroelectronics: The subsidiary signed a strategic cooperation agreement with an internationally renowned laser radar manufacturer.

Semitronics (300456) announced on the evening of April 1st that Celex Beijing, a holding subsidiary of the company, signed the Strategic Cooperation Framework Agreement with an internationally renowned laser radar manufacturer and its subsidiaries. Celex Beijing will establish and maintain an 8-inch wafer mass production line for MEMS micro-mirror products according to the process requirements provided by its cooperative customers, and provide supporting and stable production capacity according to the production capacity requirements of its cooperative customers.

Shuobeide: It is planned to transfer 51% equity of Shuobeide Communication.

Shuobeide (300322) announced on the evening of April 1 that the company transferred 51% equity of Suzhou Shuobeide Communication Technology Co., Ltd. (hereinafter referred to as "Shuobeide Communication") to Huangyuan for 42.9273 million yuan. After the transfer is completed, the company no longer holds the equity of Shuobeide Communication. Shuobeide Communication is mainly engaged in the R&D and sales of metal connecting shrapnel, die-cutting parts and other products, and the existing business is not highly synergistic with the company’s main business.

Tianlong shares: it is planned to subscribe for fund shares to invest in Yuexin Semiconductor.

Tianlong Co., Ltd. (603266) announced on the evening of April 1 that the company signed a Partnership Agreement with Shanghai SAIC Hengxu Investment Management Co., Ltd. and other relevant parties, and planned to subscribe for the fund share of Jiaxing Juanman Equity Investment Partnership (Limited Partnership). As a limited partner, the company subscribed 50 million yuan, accounting for 14.06% of the total subscribed capital contribution. The partnership intends to invest in Guangzhou Yuexin Semiconductor Technology Co., Ltd.. Guangzhou Yuexin Semiconductor Technology Co., Ltd. currently has the only production line in Guangzhou for mass production of 12-inch analog chips and power devices.

Yunnan Nengtou: Winning the bid for the photovoltaic development project in Xinping County.

Yunnan Nengtou (002053) announced on the evening of April 1 that the company had received the Notice of Winning Bid issued by the tendering agency. The company was the winning bidder of two photovoltaic development projects in Xinping County, namely Yulongzhai photovoltaic project and distributed photovoltaic project on the roof of the whole county, with an estimated total investment of 258 million yuan.

Anning Co., Ltd.: It is planned to invest 10 billion yuan to build a whole industrial chain project with an annual output of 60,000 tons of energy-grade titanium materials.

Anning Co., Ltd. (002978) announced on the evening of April 1 that recently, the company signed the Investment Contract for the Whole Industry Chain Project of Sichuan Anning Iron and Titanium Co., Ltd. with an annual output of 60,000 tons of energy-grade titanium (alloy) materials with the Management Committee of Panzhihua Vanadium and Titanium High-tech Industrial Development Zone. The total planned investment budget of the project is 10 billion yuan.

Shenzhen Energy: It is planned to invest 2.399 billion yuan in Shenzhen Guangming Energy Ecological Park Project.

Shenzhen Energy (000027) announced on the evening of April 1 that the company’s holding subsidiary, Environmental Protection Company, through its wholly-owned subsidiary, Guangming Environmental Protection Company, participated in the recruitment of the franchise of the Guangming Energy Ecological Park project in Shenzhen, Guangdong Province, and was informed of the winning bid. The total processing scale of the project is 2,250 tons/day, the construction scale of this phase is 1,500 tons/day, and the total planned investment is 2.399 billion yuan.

Qinglong Pipe Industry: The holding subsidiary won the bid of 249 million yuan.

Qinglong Pipe Industry (002457) announced on the evening of April 1st that recently, Ningxia Water Conservancy and Hydropower Survey & Design Institute Co., Ltd., a holding subsidiary of the company, won the bid for the general contracting (EPC) project of Ningdong water supply source project and water distribution network safety improvement project, with a bid amount of 249 million yuan, accounting for 10.22% of the company’s total operating income in 2021, which is expected to have a certain impact on the company’s performance from 2022 to 2024.

Far East: In March, the subsidiaries won a total bid of about 2.167 billion yuan.

Far East Co., Ltd. (600869) announced on the evening of April 1 that in March, it received a total of 2.167 billion yuan of contract orders from subsidiaries that won the bid/signed more than 10 million yuan.

Ropes Jin: The holding subsidiary pre-won the bid of 72.75 million yuan for the project.

Ropes Jin (002333) announced on the evening of April 1 that Zhongyifeng Technology, a holding subsidiary of the company, was identified as the first successful candidate for the intelligent project of Jinjihu Tunnel in Suzhou Industrial Park, with a bid price of 72,751,200 yuan.

[others]

Hengrui Pharma: Clinical trial of HRX0701 tablets was approved.

Hengrui Pharma (600276) announced on the evening of April 1st that recently, its subsidiary Shandong Shengdi Pharmaceutical received the Notice of Approval for Drug Clinical Trial on HRX0701 Tablets approved by National Medical Products Administration, and will conduct clinical trials in the near future.

Tailin Bio: The future sales business of NC membrane is uncertain.

Tailin Bio (300813) announced on the evening of April 1 that the company completed the development of NC film and the construction of production line in March this year, and officially put it into small batch production. However, at present, the production capacity of NC membrane is still very small, and the follow-up production site expansion and equipment introduction are still in progress. In the short term, the production capacity is limited, and the sales of NC membrane have just begun, accounting for a very low proportion of the company’s overall sales; At the same time, due to the short time to market of new NC film products, the brand influence is small; In addition, the market demand of NC membrane is easily affected by factors such as epidemic fluctuation, and the future sales business is uncertain.

Cryogenic shares: The short name of the securities was changed to "Shudao Equipment" from April 6th.

Cryogenic Co., Ltd. (300540) announced on the evening of April 1 that since April 6, the short name of the company’s securities has been changed to "Shudao Equipment".

Yi Yatong: It is planned to transfer 40% equity of Yi Yatong Logistics by listing.

Yi Yatong (002183) announced on the evening of April 1 that the company intends to transfer 40% equity of its wholly-owned subsidiary Yi Yatong Logistics, with a reserve price of 60 million yuan. After the transfer is completed, the company still holds 60% equity of Yiyatong Logistics.

Guilin sanjin: BC008 antibody injection has obtained implied permission for drug clinical trials.

Guilin sanjin (002275) announced on the evening of April 1st that recently, Baochuan Bio, the holding company of Sun Company, obtained the approval notice of clinical trial of BC008 antibody injection approved and issued by National Medical Products Administration, but due to the epidemic control in Shanghai, Baochuan Bio was temporarily unable to get the text information of the approval notice of clinical trial. BC008 antibody injection will be used in clinical trials for the treatment of CLDN18.2 positive advanced solid tumors.

Buchang Pharmaceutical: The clinical trial of BC004 for injection was approved.

Buchang Pharmaceutical (603858) announced on the evening of April 1st that Sichuan Luzhou Buchang Bio-Pharmaceutical, a holding subsidiary, recently received the Notice of Approval for Clinical Trials of Drugs about BC004 for Injection approved and issued by National Medical Products Administration. BC004 for injection is mainly used to treat advanced solid tumors with HER2 positive, including HER2 positive breast cancer and adenocarcinoma at the junction of gastric cancer and gastroesophagus. At present, there are no drugs with the same target listed at home and abroad.

Shen Tianma A: The wholly-owned subsidiary received 100 million yuan from the government.

Shen Tianma A (000050) announced on the evening of April 1 that recently, Xiamen Tianma, a wholly-owned subsidiary of the company, received 100 million yuan of R&D support subsidies from the management committee of Xiamen Torch High-tech Industrial Development Zone, accounting for 6.48% of the company’s net profit in 2021, and it is estimated that the total profit in 2022 will increase by 100 million yuan (unaudited).

Asia-Pacific Pharmaceutical: Omeprazole sodium for injection passed the consistency evaluation of generic drugs.

Asia-Pacific Pharmaceutical (002370) announced on the evening of April 1 that the company’s omeprazole sodium for injection passed the consistency evaluation of generic drug quality and efficacy.

Hysco: Arginine Glutamate Injection passed the consistency evaluation of generic drugs.

Haisike (002653) announced on the evening of April 1 that the arginine glutamic acid injection of Liaoning Haisike Pharmaceutical, a wholly-owned subsidiary of the company, passed the conformity evaluation of generic drugs. Arginine glutamic acid injection is a national medical insurance drug, which is mainly used for the adjuvant treatment of blood ammonia elevation caused by chronic liver disease.

Jinpu Titanium Industry: The subsidiary temporarily stopped production due to the epidemic situation.

Jinpu Titanium Industry (000545) announced on the evening of April 1 that Xuzhou Titanium Dioxide, a subsidiary of the company, will organize orderly and safe parking according to the regulations today. The time to resume normal production and operation will be arranged according to the requirements of the local government for epidemic control. The temporary shutdown of Xuzhou Titanium Dioxide is a short-term measure affected by the epidemic situation and will not adversely affect the long-term development of the company.

[Increase, decrease and repurchase]

Midea Group: It has spent 580 million yuan to buy back 10,154,200 shares.

Midea Group (000333) announced on the evening of April 1 that as of March 31, the company had bought back 10,154,200 shares by centralized bidding, accounting for 0.1452% of the company’s total share capital. The highest transaction price was 59 yuan/share, and the lowest transaction price was 54.4 yuan/share, with a total payment of 580 million yuan (excluding transaction costs).

SF Holdings: It has spent 1.287 billion yuan to buy back 24.5217 million shares.

SF Holdings (002352) announced on the evening of April 1 that as of March 31, the company had bought back 24,521,700 shares by centralized bidding (accounting for 0.5% of the company’s total share capital at present), and the repurchase funds were about 1,287 million yuan (excluding transaction costs), with an average transaction price of 52.48 yuan/share (the highest transaction price was 59.4 yuan/share and the lowest transaction price was 46.77).

Online and offline: Yijian Investment intends to reduce its shareholding by no more than 6%.

Online and offline (300959) announced on the evening of April 1st that Yi Jian Investment, a shareholder holding 10.27%, plans to reduce its holdings by no more than 4.8 million shares (accounting for 6% of the company’s total share capital) through centralized bidding or block trading from April 27th to August 26th.

Yueling shares: the actual controller and shareholders intend to reduce their holdings by no more than 2.93% in total.

Yueling Co., Ltd. (002725) announced on the evening of April 1 that Lin Wanqing, one of the controlling shareholders and actual controllers of the company, and Zhong Xiaotou, a shareholder holding more than 5% of the shares, intend to reduce their holdings by no more than 2.93%.

Dinglong Culture: The two shareholders intend to reduce their holdings by no more than 5.49% in total.

Dinglong Culture (002502) announced on the evening of April 1st that the shareholders Qingdao Henglan Investment Co., Ltd. and Zhuhai Haohui Investment Co., Ltd. plan to reduce their shares by no more than 50,545,800 shares (accounting for 5.49% of the total shares of the company).

Huaping shares: the shareholders intend to reduce the company’s shares by no more than 3%.

Huaping (300074) announced on the evening of April 1 that Xiong Mochang, a shareholder holding more than 5% of the company’s shares, plans to reduce the company’s shares by no more than 16,016,800 shares (accounting for 3% of the company’s total share capital) through centralized bidding and block trading.

Harmo Science and Technology: The actual controller and its concerted parties intend to reduce their holdings by no more than 5.23%.

Harmo Science and Technology (300084) announced on the evening of April 1 that Dou Jianwen, the controlling shareholder and actual controller of the company, and Zhang Ligang, the concerted action person of the company, plan to reduce their holdings by no more than 5.23% through centralized bidding, block trading and agreement transfer.

China Mining Resources: Some directors and senior executives plan to reduce their holdings by no more than 1.05%.

China Mining Resources (002738) announced on the evening of April 1 that some directors and senior executives plan to reduce their holdings by block trading or centralized bidding within six months after 15 trading days, accounting for 1.05% of the company’s total share capital.

Chujiang New Materials: Some directors and their concerted actions and supervisors intend to reduce their shares.

Chujiang New Materials (002171) announced on the evening of April 1 that Miao Yunliang, the company’s director, Cao Wenyu, the company’s concerted action, and Cao Quanzhong, the company’s supervisor, plan to reduce their holdings by no more than 2.13% in the six months after 15 trading days.

Hailian Jinhui: UnionPay intends to reduce its shareholding by no more than 1%.

Hailian Jinhui (002537) announced on the evening of April 1st that UnionPay, a shareholder holding 7.13% of the shares, plans to reduce its shareholding by no more than 11.74 million shares (about 1% of the company’s total share capital) within three months after 15 trading days.